The Hidden Forces Behind Your Financial Decisions: How Psychology Shapes the Markets

Author : Kusum Lamsal

Date: January 21, 2025

Introduction:

Have you ever made a financial decision that left you wondering, What was I thinking? Maybe you splurged on something unnecessary, clung to a losing investment, or hesitated to spend money you’d worked hard to earn. These seemingly irrational choices aren’t just personal quirks—they’re deeply tied to our psychology. This is where behavioral finance comes into play, blending economics and psychology to explore how emotions and biases influence our financial decisions.

In this blog, we’ll delve into the fascinating world of behavioral finance, uncovering how it impacts our daily lives, from saving and spending to investing. Let’s explore the hidden forces shaping our financial behaviors—and how we can take control.

Understanding Behavioral Finance

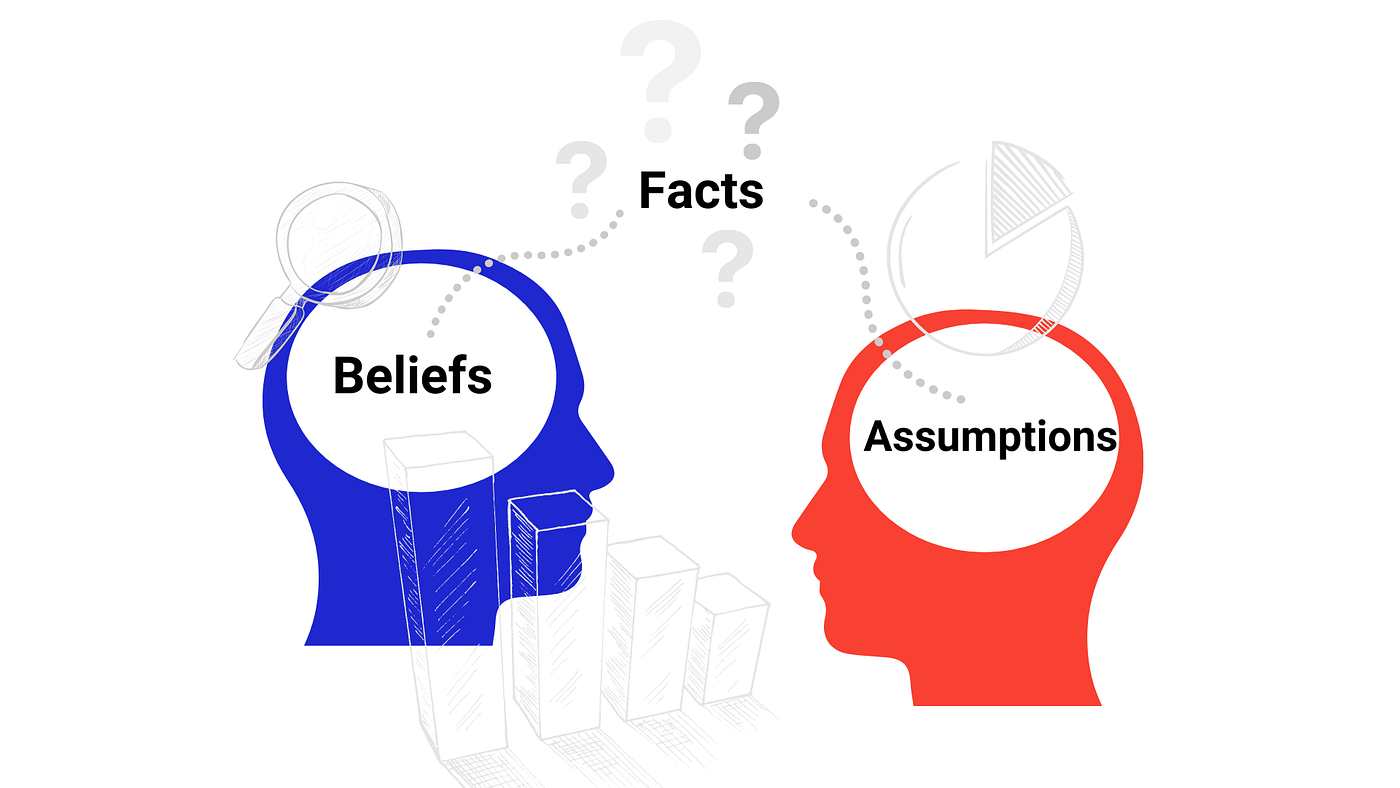

At its core, behavioral finance examines how psychological factors influence economic decisions. Unlike traditional finance, which assumes people are rational and logical, behavioral finance acknowledges that we are often driven by emotions, biases, and cognitive shortcuts.

For instance, fear and greed are powerful motivators in the stock market. A fearful investor might sell their stocks too early, fearing further losses, while a greedy one might hold on too long, hoping for endless gains, only to face disappointment when the market crashes. These behaviors demonstrate how human emotions often clash with rational decision-making. Figure: Behavioral Finance simple diagram

Cognitive Biases and Real-Life Examples

Behavioral finance is rooted in the study of cognitive biases—mental shortcuts that influence our judgment. Here are some common biases, illustrated with relatable examples:  Figure : Cognitive Bias

Figure : Cognitive Bias

Loss Aversion: We tend to feel the pain of loss more intensely than the joy of gain. For example, when we lose even a small amount of hard-earned money, it can weigh on our minds all day. On the flip side, if we stumble upon found money, like cash on the street, we’re more likely to spend it freely without much thought.

Mental Accounting: The value we assign to money depends on its source. Hard-earned money from a job feels more valuable, so we’re cautious about spending it. However, money won in a card game or lottery feels like a bonus, making us more inclined to spend it frivolously.

Overconfidence Bias: People often overestimate their ability to predict financial outcomes. This overconfidence can lead to risky investments, assuming we have more control or insight than we actually do.

Anchoring: Our decisions are often influenced by initial reference points. For instance, during sales, we focus on the “discounted” price rather than whether we actually need the product.

The Role of Modern Financial Systems

The rise of digital banking and cashless transactions has also shaped our financial behaviors. With digital payments, we’re less likely to feel the “pain” of spending compared to dealing with physical cash. Handing over cash creates a tangible connection to our spending, making us more mindful of our financial choices. Digital systems, while convenient, can sometimes encourage overspending because they reduce this emotional friction.

Figure : Digital wallets

Figure : Digital wallets

The Psychology-Finance Connection and Ongoing Research

Behavioral finance bridges the gap between the actual (normal) behaviors of individuals and the expected (rational) behaviors predicted by traditional economics. While the field has made significant strides in identifying biases and their effects, psychologists and economists are still working on creating a standardized framework to benchmark these relationships. Innovations and research are ongoing to deepen our understanding of the interplay between psychology and financial decision-making.

Overcoming Psychological Traps

Awareness is the first step toward better financial decisions. Here are some tips to avoid falling into common psychological traps:

Track Spending: Whether it’s cash or digital, keeping a record of expenses can help you remain mindful of your financial habits.

Figure : Representative image of expenditure spending tracking

Figure : Representative image of expenditure spending trackingSet Goals: Clear, long-term financial goals provide direction and reduce impulsive decisions.

Seek Advice: A trusted financial advisor or mentor can offer an objective perspective to counteract emotional decision-making.

Pause and Reflect: Before making a financial decision, take a moment to consider if it’s driven by logic or emotion.

Real-Life Examples of Behavioral Finance Biases

Disposition Effect in Stock Trading

We have seen investors often sell assets that have recently increased in value but holding to those depricated assets in hope of rebound

Example: An investor sells a stock that has gained 20% quickly to “lock in gains” but holds onto a stock that has lost 20%, expecting it to recover, which may lead to larger losses.Overconfidence Bias in Trading

Traders often overestimate their ability to predict market movements sometimes leading to excessive trading or some potential lossesExample: A day trader believes they can consistently outperform the market based on personal analysis, resulting in frequent trades that incur high fees and underperformance.

Status Quo Bias in Retirement Plans

People often stick with default investment options for their retirement plans ,even when better option are available in the marketExample: An employee enrolls in a retirement plan and remains with the default conservative investment fund (Sanchay Kosh), missing out on higher returns from a more aggressive portfolio suitable for their age and retirement timeline.

Present Bias in Savings Behavior

Priotizing immediate gratification over long-term benefits can lead to insufficient savingsExample: Choosing to spend discretionary income on luxury items now rather than saving for future financial security, resulting in inadequate retirement funds.

Herd Behavior in Cryptocurrency Investments

Majority in cryptocurrency trade without conducting personal research , driven by the fear of missing out , this was seen in case of NFTs trading in 2020s as wellExample: During the 2017 Bitcoin surge and 2020s NFT and then meme cryptocoins, many individuals invested solely because others were doing so, leading to a bubble that eventually burst.

Credit Card Rewards and Mental Accounting

Consumers often perceive rewards points or miles as “free money,” leading them to spend more freely than they would with cash.Example: A person might choose a more expensive flight or hotel simply because they can pay with accumulated points and Spending more than they can and enjoying luxury on credit cards because they think they can pay later while disregarding the working of credit systems

Conclusion :

Behavioral finance reveals the profound impact of psychology on our financial lives. From the cautious spending of hard-earned money to the carefree use of found cash, our decisions are shaped by a mix of emotions, biases, and cognitive tendencies. As the field continues to evolve, it challenges us to examine the hidden forces behind our financial behaviors—and to strive for a balance between the rational and the emotional.

By understanding and addressing these psychological factors, we can make smarter, more intentional financial decisions, improving both our economic outcomes and our peace of mind.